Make money for yourself: banks raised loan rates ahead of expected key rate cut

Banks have increased the average level of the total cost of loans, despite the expected decrease in the key one, Izvestia found out. The indicator increased by 1 percentage point, to 35%. More than half of the top 10 players significantly raised the upper limit of the range, which is why loans on average rose in price, despite the apparent reduction in rates. Credit organizations are trying to make money on customers who are willing to take out expensive loans, before the key is lowered even more — to 18%. To whom loans are being approved now, see the Izvestia article.

How much have loans become more expensive

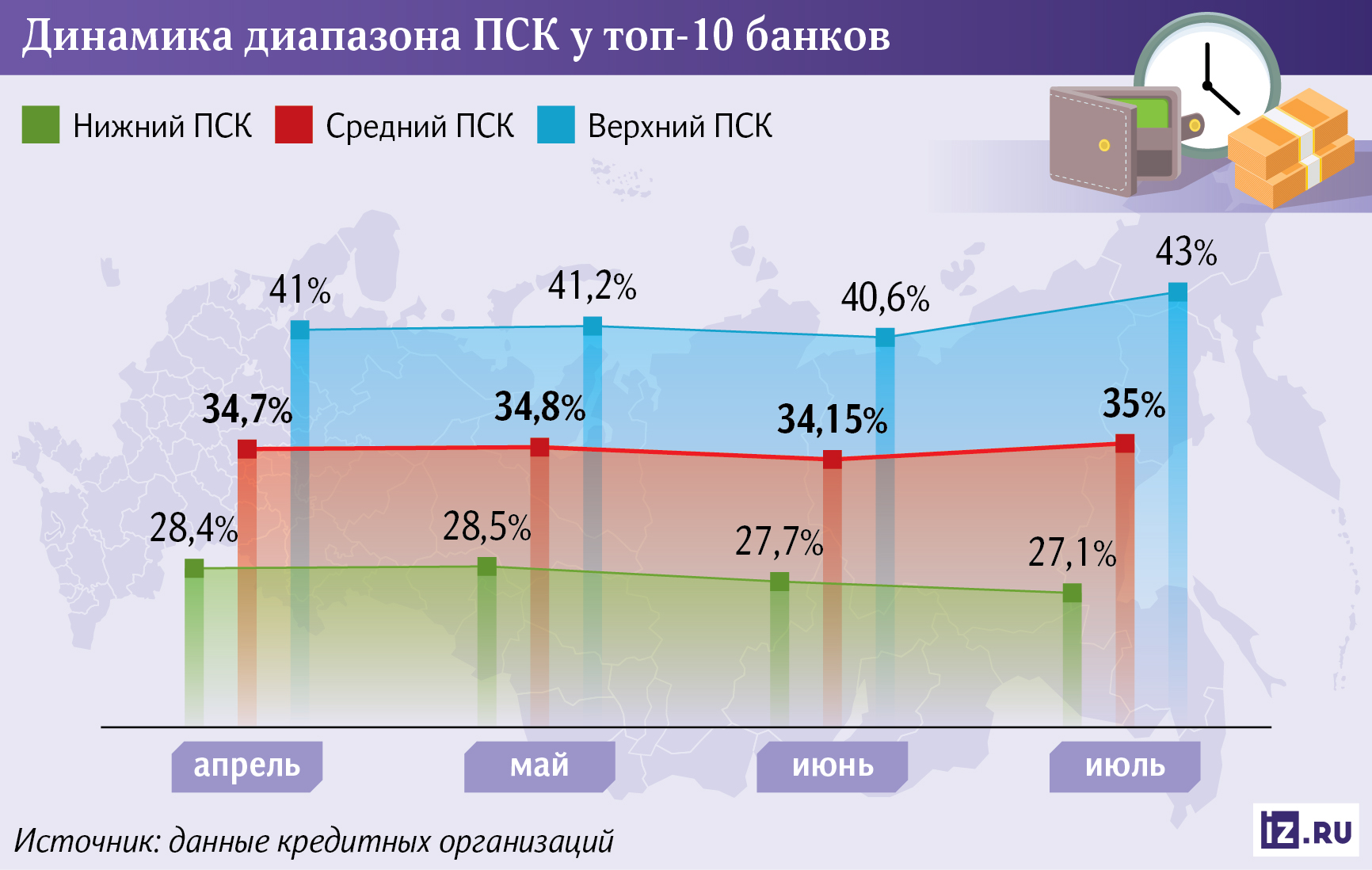

Banks have expanded the ranges of full—cost loans - the average rate level has increased for six of the top 10 market participants by almost 1 percentage point. New loans will be issued at an average of 35%, according to data from their websites, which were studied by Izvestia. This is happening despite the reduction of the key rate to 20% at the last meeting and expectations of an even greater easing of the regulator's policy on July 25.

The UC includes all expenses that the borrower pays during the loan period. In addition to the rate, it is usually also the cost of insurance and commissions — for servicing, maintaining the borrower's accounts, issuing cards, and other additional services.

Almost half of the banks over the past month lowered the lower limit of the CPI for consumer loans — it reached 26.4% for the largest market players, according to data from their websites. However, most of them also raised the cost of borrowing for the riskiest borrowers — the upper limit of the CPI increased by almost 2.5 percentage points and reached 43%.

Banks issue loans closer to the middle of this range. The average level of the full cost of loans already issued was an impressive 33.6%, according to data from the United Credit Bureau (OKB). Compared to the previous month, it fell by 0.8 percentage points. The National Bureau of Credit Histories (NBKI) also confirmed that the CPI for loans issued decreased for the third month after the peak in March.

However, the problem is that these loans are now being given only to the most solvent customers who are willing to afford an expensive loan, said economist Andrei Barkhota. At the same time, for an average borrower, an increase in the average CPI in any case means an increase in the cost of loans. Lending remains too expensive for most customers.

This is confirmed by the fact that the share of approved applications for consumer loans has been in the range of 22-24% since March, according to NBKI data. Banks reject three out of four borrowers, which means that they tend to give loans not to "average" ones, but to more financially stable ones.

The lowest rates are offered to people with a high credit rating, stable income and no delinquencies, explained Magomed Gamzaev, director of the credit department at Compare. The least risky segment for a financial organization is its existing customers, preferably those who receive a salary to an account with the organization, said the head of expert analytics at Banks.<url>" by Inna Soldatenkova.

"Loans at the upper limit of the UCS occupy an insignificant share and are issued within the framework of the risk appetite established in the bank," added the Director of Retail products at Dom Bank.Russian Federation" by Daria Morozova.

At the same time, an ordinary borrower is likely to accept any terms of the bank if he really needs money, said Natalia Milchakova, a leading analyst at Freedom Finance Global. Despite the fact that lending is becoming more expensive for him, he has no choice, because the rates of most banks are about the same. And in places where loans are cheaper, such a borrower is more likely to face a refusal on the application, Andrei Barkhota added.

Why banks don't lower their borrowing rates

Usually, expensive loans are given for a short period of time or for a small amount, for example, before paycheck or for urgent purchases, explained Dmitry Dolzhenko, head of consumer credit development at Ingo Bank. And although the interest on them is high, in terms of money, the overpayment is not so large, because the term is short and the amount of debt is small.

The increase in interest rates allows banks to approve loan applications for more risky borrowers, Dmitry Dolzhenko noted. According to him, the growth of the average CPC means that market players want to expand the number of customer segments available to them by attracting risky borrowers.

Overdue loans have been in the "red zone" since April, economist Andrei Barkhota recalled. Izvestia wrote about this — by the end of May, the volume of overdue loans to individuals reached a record 1.5 trillion rubles.

— All this indicates an increase in the risks of conventional consumer loans. This is the main reason why banks are not reducing, but increasing, the average CPI on loans," the expert explained.

Income growth is slowing down as the shortage of people in the labor market resolves, said Boris Kopeikin, chief economist at the Stolypin Institute for Growth Economics. Previously, due to the shortage of labor resources, salaries in certain industries grew at a faster pace, but now the situation has changed. This is a factor in favor of an increase in loan delinquencies. Banks will be forced to take into account the growing risks of non-repayment of loans at interest, the expert emphasized.

Banks issue loans for the money they attract through deposits, and their profitability directly affects the cost of loans. In addition, additional reserves have to be allocated for overdue loans — this is money that "does not work", but still costs the bank dearly.

Market players reduce deposit yields quickly, often even before the actual reduction in the key rate, explained Natalia Milchakova, a leading analyst at Freedom Finance Global. But the interest on loans falls with a delay of several weeks. To maintain profits, banks wait until payments on old expensive deposits are over, and only then lower loan rates.

It turns out that market participants are currently in very favorable conditions. Even Russian President Vladimir Putin noted that the margin of Russian banks has reached 5.7%, which is one and a half times higher than that of foreign credit institutions.

In addition, the CPI includes the cost of insurance products, which are often issued together with loans, Natalia Milchakova added. Insurers, in principle, are in no hurry to reduce prices following the key one — this is also a factor in favor of keeping the full cost at current levels.

Nevertheless, in the future, real rates will still begin to decrease, the expert concluded. Banks will have to adapt to the new market conditions in order not to lose the competition to other players. Conditions for borrowers with a good credit history and transparent incomes will improve faster — in the near future.

Переведено сервисом «Яндекс Переводчик»